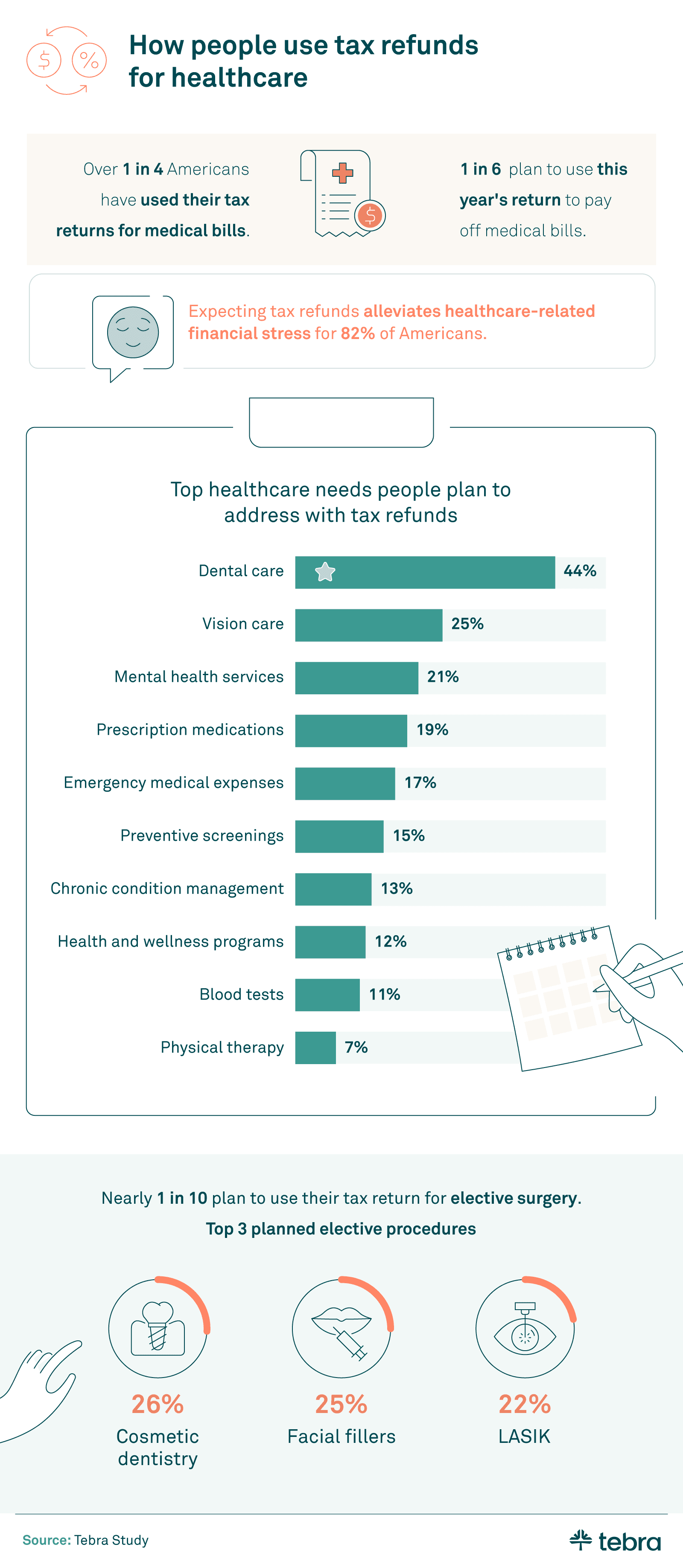

- More than 1 in 4 people report using a tax return for medical bills.

- 1 in 6 expect to put this year’s refund toward paying off medical bills.

- Nearly 1 in 10 plan to use a refund for elective surgery.

- Many direct refunds to essentials like dental care, vision care, and mental health services.

- 82% say knowing a refund is coming reduces stress.

- Private practices may see steadier appointment follow-through when refunds arrive, as patients catch up on bills and routine care.

Each year, as tax season winds down, anticipation builds for refunds. Many people still use them to save or pay down debt, while others rely on that money to cover health insurance coverage and everyday health care coverage costs. Recent reporting from Bankrate and Experian shows a large share plans to channel refunds toward savings or debt reduction.

Under the Affordable Care Act, Marketplace enrollees may qualify for help with their monthly premiums through the health insurance marketplace. Those savings are reconciled at tax time, which is one reason refunds feel closely tied to rising health insurance premiums.

In this piece, you will see how refunds intersect with medical bills, how people prioritize care when money is tight, and what our new survey suggests about the role of refunds across different household income levels. We keep the focus on practical choices people make to stay insured and keep up with care.

To ascertain the current state of tax refunds and patients, Tebra surveyed 1,000 Americans to investigate how they plan to use tax refunds to help with medical expenses.

Turning tax refunds into healthcare relief

Navigating personal finance is hard when healthcare expenses keep climbing. Many people route refunds toward care to avoid delaying appointments or prescriptions. It’s a practical choice that helps families keep health coverage intact when budgets are tight.

What our survey shows

More than 1 in 4 Americans have used a refund to pay medical bills. For some, this year’s tax return is already set aside for outstanding balances, with 1 in 6 planning to do the same. Our survey also found that 20% of Gen Z respondents expect to use refunds for medical bills.

A majority of Americans, 82%, say the expectation of a refund lowers stress. Many plan to direct funds to essentials first, including dental care (44%), vision care (25%), and mental health services (21%). Nearly 1 in 10 plan to put money toward elective procedures such as cosmetic dentistry, facial fillers, or LASIK.

Top 5 states planning to use tax returns to pay off medical bills, by percentage of respondents:

- Illinois (21%)

- Ohio (18%)

- Virginia (17%)

- Texas (17%)

- Pennsylvania (16%)

Top 5 states planning to use tax returns for elective procedures, by percentage of respondents:

- Florida (9%)

- New York (12%)

- Virginia (12%)

- Illinois (11%)

- Texas (10%)

Why refunds get pulled into care now

National estimates point to higher overall spending and continued growth in out-of-pocket costs, which can push refunds toward copays, deductibles, and a plan premium that inches higher. CMS’s national health expenditure fact sheet and the broader NHE data resource show the pressure households feel during tax time.

Medical debt and everyday essentials

Cost worries shape choices about checkups, prescriptions, and timing. KFF research on Americans’ challenges with health care costs found that about 4 in 10 adults report debt tied to medical or dental bills.

A related KFF quick take on medical debt polling notes roughly 1 in 4 have bills that are past due or that they cannot pay. That’s why many refunds go first to essentials like dental care, vision care, and mental health services before anything discretionary.

Quick ACA terms tied to refunds

Under the Affordable Care Act, the IRS premium tax credit (PTC) helps eligible enrollees lower their monthly premiums. When advance payments of the premium tax credit (APTC) are made during the year, taxpayers reconcile them on an income tax return by filing Form 8962 and referencing the official Form 8962 instructions.

Details on Form 1095-A, the health insurance marketplace statement, and the second-lowest-cost Silver plan baseline appear in Healthcare.gov’s page on Marketplace taxes and reconciliation. Depending on reported income and coverage details, reconciliation can increase a refund, reduce it, or trigger repayment.

Eligibility signals readers ask about

Eligibility turns on household income, filing status, family size, and placement relative to the federal poverty line. Current thresholds in the ASPE 2025 poverty guidelines and the Healthcare.gov glossary entry for the federal poverty level frame typical eligibility discussions.

Special rules can apply to married filing separately, while Medicaid and Medicare status may shape options during a coverage year. Some plans’ cost-sharing features (deductibles, copays) also influence which services people schedule first.

Behavior we observed in the survey

Respondents said the expectation of a refund reduces stress, as it makes it easier to book appointments and catch up on balances. Many plan to prioritize dental care, vision care, and mental health services. Nearly 1 in 10 expect to use funds for elective procedures, including cosmetic dentistry, facial fillers, and LASIK, once essential bills are addressed.

How people prioritize care when refunds are limited

When money is tight, people rank care by urgency and out-of-pocket cost. Routine cleanings or glasses often come first because prices are predictable. Specialist visits may wait until a balance is cleared.

A modest refund can cover a deductible on dental care or a few therapy sessions for mental health services. If a prescription is needed, families often use the refund to refill for several months and avoid gaps.

Those choices keep health coverage useful while stretching every dollar. Even a partial payment on medical bills helps people stay current with statements and lowers the risk of collections. That’s why refunds so often land on essentials before elective care and why small timing differences around tax time matter for scheduling.

Two quick scenarios people mention in surveys

A parent who delayed an eye exam uses part of a refund to update lenses and pay a past-due balance for vision care. The rest goes to a primary care follow-up that was rescheduled twice. Another household puts the first dollars toward a lingering imaging bill, then books a therapist intake once the account shows paid.

If money remains, they reserve a slot for dental care to fix a cracked filling. Elective procedures return to the list only after the essentials are covered. These tradeoffs are common when a plan's premium, copays, and prescriptions all draw from the same budget. A refund doesn’t solve everything, but it keeps care moving and prevents small problems from turning into bigger medical bills.

What this means for private practices

Refund season often coincides with patients settling balances and scheduling overdue visits. Practices can meet that moment with clear estimates, flexible options, and courteous reminders. Integrated tools for statements and patient payments inside modern EHR software and Tebra’s patient payments capabilities make it simpler for teams to provide accurate amounts and for patients to pay without delay.

Teams can plan for the refund window with small operational tweaks. Post clear timeframes for statements, add gentle reminders before tax time, and train front-desk staff on plain-language estimates.

Consider a short script that explains how patient payments work when a balance remains after insurance. Where possible, present a single number that reflects expected benefits and likely monthly payments. Those steps keep conversations simple and respectful. They also reduce back-and-forth during busy weeks when many families are deciding how to split a refund across bills.

Healthcare finance and tax refunds

The latest IRS filing season snapshot shows how refunds were issued for tax year 2024 returns processed during early 2025. As of the week ending May 9, 2025, the IRS reported 145.9 million returns received, 143.6 million processed, 93.6 million refunds issued, and $274.98 billion refunded.

The average tax refund reached $2,939, with 86.9 million direct deposits averaging $3,034. Speed at tax time matters. Electronic filing with direct deposit generally arrives faster than paper returns and checks, which helps families line up spring bills, premiums, and monthly payments without delay.

How reconciliation can change a refund

Marketplace enrollees often lower their monthly premiums during the year with the premium tax credit. At filing, taxpayers reconcile advance amounts using Form 1095-A and complete Form 8962 as part of an individual income tax return or federal income tax return.

Depending on income and coverage details, that calculation can increase a refund, reduce it, or create a repayment. Healthcare.gov explains the mechanics of Marketplace taxes and reconciliation.

Readers may still encounter legacy terms across tax forms, including the individual shared responsibility provision and minimum essential coverage, which appear in glossaries for historical context.

For private practices, timing has practical implications. When refunds land, many patients clear balances or book care they postponed.

Clear estimates and predictable bills help set expectations. Teams can also use more flexible payment plans or better healthcare price transparency to present upfront ranges and reduce surprises in the patient journey.

Aligning statements with refund timing, offering simple payment plans, and supporting online checkout can also help manage a tax liability that emerges during reconciliation while keeping medical bills on track.

Methodology

Tebra surveyed 1,000 taxpayers in January 2024 to understand how tax refunds support medical expenses during a given coverage year. Respondents included 14% Gen Z, 58% Millennials, 24% Gen X, and 4% Baby Boomers. State-level findings were reported only for states with 50 or more respondents.

The survey captured planned uses of refunds for medical bills, including essentials such as dental, vision, and mental health care, as well as select elective procedures. To provide context around spending and affordability, any third-party figures referenced in this article are current to 2024–2025 and come from authoritative sources such as the IRS, CMS, KFF, and Healthcare.gov.

About Tebra

Tebra, headquartered in Southern California, empowers independent healthcare practices with cutting-edge AI and automation to drive growth, streamline care, and boost efficiency. Our all-in-one EHR and billing platform delivers everything you need to attract and engage your patients, including online scheduling, reputation management, and digital communications.

Inspired by "vertebrae," our name embodies our mission to be the backbone of healthcare success. With over 165,000 providers and 190 million patient records, Tebra is redefining healthcare through innovation and a commitment to customer success. We're not just optimizing operations — we're ensuring private practices thrive.

Fair use statement

You may share these findings for noncommercial use with proper attribution. Please include a link back to this page so readers can access the full context, methodology, and sources. Attribution helps preserve accuracy for anyone citing or referencing the content.

FAQs

Common questions about refunds and healthcare

- Current Version – Nov 17, 2025Written by: Jean LeeChanges: This article was updated to include the most relevant and up-to-date information available.